Oct 23, 2019

Bad News Piles up for Woodford Investors

In recent days the British news media have reported (for example here and here) that the suspended LF Woodford Equity Income Fund (WEIF), which has about 3.5 billion pounds worth of assets locked up inside it, will be liquidated, wound up and, starting from January 2020, funds returned to investors. The decision was made by the fund’s administrator Link Fund Solutions, against the wishes of the principal fund manager, Neil Woodford, who wanted the fund to continue as a going concern. In Mr Woodford’s view, “This was Link’s decision and one I cannot accept, nor believe is in the long-term interests of LF Woodford Equity Income Fund investors.”

As an immediate consequence of Link’s intervention, formerly high-flying Woodford Investment Management Limited (WIM) was sacked as the fund manager. The dismissal was costly to WIM, as it stood to lose access to controversial fee revenues, estimated at approximately 9 million pounds charged to WEIF investors alone since fund suspension was imposed at the beginning of June 2019. As a knock on effect, Mr Woodford decided to terminate WIM’s services to the other Woodford-branded funds and close his eponymous funds management business.

In the previous edition of The Supervisor we published twin articles on the liquidity mismatch crisis that egulfed WEIF and the related Woodford Equity Income Feeder Fund (WEIFF). The bitter end for the now-notorious Woodford retail financial products arose from a slow-moving collision of poor fund performance, increasingly high investor withdrawal rates, and illiquidity in a significant proportion of fund assets. At a certain point the funds were not able to meet redemption requests without prejudicing the interests of remaining investors. The last pricing for trades in WEIF occurred at midday Friday, 31 May 2019. From Monday, June 3 2019, unit trading suspension set in when the embattled funds were “gated”, meaning closed to investor transactions until further notice.

WEIF is now engaged in a costly and protracted asset restructuring and winding up process. Before Link stepped in to put it out of its misery, WEIF was already beset by deteriorating loss in fund value, forced sale of illiquid assets at adverse prices, ongoing purchase of liquid but lower-returning replacement assets, periodic calls to fund previous venture capital commitments, and WIM’s ongoing management fees. Investors trapped in the fund will not be pleased to learn from the newest development that, at the earliest, projected completion of their repayments will occur at some unspecified time next year.

The Woodford saga has achieved the dubious distinction of having its own dedicated news threads, such as the one on Wealth Manager operated by CityWire.

Demands Intensify for Changes to how Open-ended Funds are Operated

In the wake of the Woodford funds debacle, Bank of England (BoE) governor Mark Carney has reiterated his criticism of the way the funds were structured, but was careful to disavow any responsibility on behalf of his institution:

“There is a structural problem in open-ended funds. A problem that is not our direct responsibility but a problem in terms of fairness for the individuals who invest in these [funds].”

Mr Carney characterised the Woodford affair as a “consumer protection issue” in contrast to the way in which the BoE “comes at it from a system perspective and how this could impact the functioning of the system, and ultimately the ability of the system to fund growth in the economy.”

The same article quoted UK Treasury Committee interim chair Catherine McKinnell as implying that new regulation would be needed:

“There is still some time to go in this uncomfortable episode, which has raised important questions about the functioning of the funds industry.”

The Daily Mail quoted Ben Yearsley, director of Shore Financial Planning, arguing for increased regulation through outright banning of unlisted securities from normal retail managed funds:

“In my view, this just shows that unquoted holdings shouldn't be held in open ended funds. The Financial Conduct Authority should now look at this and go further than they went recently to ensure this can't happen again and essentially outlaw unlisted holdings from the open ended fund structure.”

British Regulators get a Move On

When the Woodford funds suspension scandal first broke, fingers were pointed at the City of London’s financial regulators, the BOE and the Financial Conduct Authority (FCA), with accusations flying about sleeping at the wheel. Matters were not helped for the FCA when it admitted in writing that it had known about and closely monitored the parlous liquidity position of WEIF well in advance of the redemption crisis that shuttered access to withdrawals indefinitely to investors.

No doubt stung by the rebukes, the two regulators have not since been idle in working on ways to prevent managed funds from doing another Woodford. This month the BoE’s Financial Policy Committee (FPC) issued a Financial Policy Summary and Record (FPSR) in which it addressed liquidity mismatches in managed funds. The BoE’s website states that the FPC “aims to ensure the UK financial system is resilient to, and prepared for, the wide range of risks it could face — so that the system can serve UK households and businesses in bad times as well as good.” Right now the FPC is understandably up to its eyeballs in Brexit emergency preparations, but it still found time to make some remarks on Woodford-style issues in funds management.

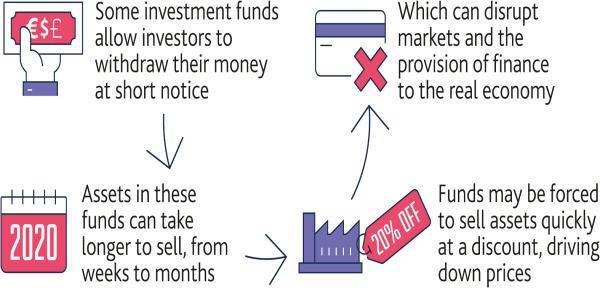

Under the heading “Tackling vulnerabilities in open-ended funds”, the FPSR summarised the core problem as, “The FPC continues to judge that the mismatch between redemption terms and the liquidity of some funds’ assets has the potential to become a systemic risk.” Accompanying this summation, the FPSR published an excellent simplified diagram that neatly encapsulates the essentials of the Woodford mess.

Figure 1: Stylised Diagram of Managed Fund Illiquidity Crisis (Source: BoE FPSC October 2019)

The FPSR set out the FCP’s analysis and action plan as follows:

“This mismatch creates incentives for investors to redeem ahead of others, which can lead to forced asset sales by funds and amplify asset price movements. Sharp falls in asset prices could increase the cost of finance to companies, leading to lower investment and output in the economy. These incentives should be reduced through greater consistency in the design of funds between:

“The Bank and the Financial Conduct Authority (FCA) are undertaking a joint review to assess how funds’ redemption terms might be better aligned with the liquidity of their assets in order to minimise financial stability risks without compromising the supply of productive finance. The progress of this review will be reported in the December Financial Stability Report (FSR).”

Thus December 2019 will be the time when the BoE and FCA jointly issue their review update on operating rules for open-ended funds. There will be four fragile pieces to juggle together in this exercise:

One can only wish the London City authorities the best of British luck in resolving this conundrum, which might prove only slightly less challenging to reconcile than looming fallout from Brexit.

FMA on the case

New Zealand’s Financial Markets Authority (FMA) will likely pay keen attention to the widely anticipated FSR communique, as it is also looking into similar types of problems that can beset managed funds.

In its Annual Corporate Plan 2019/20, the FMA states in the chapter “Investment Management”, under the heading “Sector risks and harms we want to address”, that it is concerned about:

“Stability of funds – Managed Investment Scheme (MIS) managers have insufficient processes and controls to respond to a liquidity crisis event, which could lead to investor losses.” (p. 12)

This statement (which is also repeated twice verbatim in the FMA’s Strategic Risk Outlook 2019 pp. 7, 20) points under “Activities for 2019/20” to the work objective:

“MIS stress testing – work with supervisors to test the readiness of MIS managers to respond to a liquidity crisis event.” (p. 13)

The FMA will be examining much the same interrelationships within managed funds between asset liquidity and redemption rules, and how these interconnections might cause wider knock-on disruptions in financial markets and real economies, that the BoE and the FCA are currently investigating.

It is an ill wind that blows nobody any good. The travails of Woodford fund investors may yet prove their weight in gold by helping others to avoid similar ensnarement under possible new regulations for funds management.

Thoughts from a Supervisor’s Perspective

Had the Woodford fund suspension issue arisen in New Zealand, then the FMA could expect to have been notified in the lead up to the event by the fund’s supervisor under the FMCA’s section 203. However, as noted in relation to the FCA’s role in monitoring liquidity stress in WEIF, having the regulator made aware of a problem does not necessarily of itself result in a satisfactory solution.

The governing documents of a managed fund should contain detailed provisions for what procedures must be followed in the event that allowing investors to make withdrawals could potentially prejudice the rights of other investors in the same fund, including the right to expect that the licensed manager would fully comply with its legislated duties under the FMCA’s section 143(1)(b)(i) and (ii) in weighing up whether to permit or deny withdrawal requests.

That said, if the supervisor is doing its job properly, it is the fence at the top of the cliff that also requires attention, and not just the ambulance at the bottom. The FMA expects supervisors to be proactive in identifying risks to investors before adverse consequences arise.

In the Woodford case, supposing it had arisen in New Zealand, there were potential risks evident that a proactive supervisor should have identified and brought to the fund manager’s attention for discussion and remediation. One was the fawning cult-like status afforded to WIM principal, Mr Woodford, not just by investors but also by sections of the UK news media such as the BBC. Arguably, this elevated status allowed latent problems to accumulate to crisis point in the way in which WEIF was invested. A “star” manager brings key person risks – not just in terms of sudden loss of the person concerned, but also in potential lack of curbs and controls on that person’s decisions and actions - to a funds management business that must be recognised and ameliorated.

Another potential risk lay in the manager remuneration structure of WEIF. After fund suspension, WEIF’s manager WIM did not discount its lucrative management fees and even rejected widespread suggestions from many quarters that it should do so. Arguably, WIM had a possible conflict of interest in continuing to collect its full management fees whilst advocating that WEIF should remain in permanent operation as a going concern, rather than being wound down promptly and funds returned to investors at material loss to WIM.

A further potential risk lay in the solvency of the fund manager if one of its funds had to be shut down with resulting substantial decline in the manager’s revenue. With WEIF forcibly taken out of WIM’s hands by Link, and WIM thereafter left with managing only with its embattled remaining funds, the listed Woodford Patient Capital Trust (WPCT.L) and the LF Woodford Income Focus fund, the plug was pulled in short order. WIM abruptly announced that it was closing shop, leaving investors in those other funds also in the lurch.

It would have taken farsightedness to spot the potential risks described above when the Woodford funds were in their heyday and Mr Woodford was being hailed from all sides as a Midas touch who could do no wrong. Nonetheless, the incipient problems could be discerned, at least in outline, and should have been identified for further investigation. Once the Woodford funds began performing poorly over a protracted period, eventually causing investors to stream for the exits, these risks were becoming much more apparent and needed to be addressed before it was too late to avert disaster.

While the Woodford saga plays out on the other side of the world, its ripple effects will continue to impact on regulators and supervisors in New Zealand.