Apr 19, 2024

At the beginning of April 2024, the FMA released a document entitled Consultation: Proposed exemption for certain green, social, sustainability and sustainability-linked bonds (Consultation). The Consultation is intended to update the FMA’s 2019 information sheet Green bonds – same class exclusion (Information Sheet). Both these documents are concerned with how an exemption from the requirement for debt issuers to produce a product disclosure statement (PDS) to accompany a listed bond offering to the retail marketplace might beneficially apply in New Zealand. The requirement to produce a PDS increases compliance costs for retail bond issuers. The FMA has evidently been interested in reducing compliance costs through its powers under the Financial Markets Conduct Act 2013 (FMC Act) to issue exemptions from disclosure requirements.

The Consultation goes further than the Information Sheet in a number of key ways. The latter addresses how an aspect of law – the “same class exclusion” of clause 19 of Schedule 1 of the FMC Act – might be applied to disclosure requirements for listed retail “green bonds”. The Information Sheet concludes that if such green bonds are sufficiently different from the pre-existing listed “vanilla” (ie., non-green) bonds of the same issuer, then the FMA would need to look at granting an individual exemption to allow the issuer to avoid having to produce a separate PDS for the green bonds. The Information Sheet is focused on addressing a legal technicality about how clause 19 applies in the case of listed green bonds, and not greatly with the question of how exemptions from PDS requirements might impact on the marketplace in terms of changing the overall demand and supply dynamics for such bonds.

In practice, it seems that little use has been made of individual exemptions to issue listed green bonds without a PDS, as the Consultation notes that the FMA has only granted two such exemptions within the five years since the Information Sheet was published. One exemption went to Christchurch City Holdings Limited and the other to New Zealand Local Government Funding Agency Limited. Not exactly a “big bang” in terms of listed retail green bond supply. Since it published the Information Sheet, it seems that the FMA has grown keen to chivvy things along concerning green bond issuance.

A significant departure from the stance of the Information Sheet with respect to market impacts of granting listed green bond exemptions from PDS disclosure requirements is the way in which the Consultation announces that the FMA is interested in expanding the issuance of such bonds significantly within the New Zealand marketplace. This expansion is premised upon the FMA granting a class exemption – as opposed to individual exemptions - from the PDS requirement. The regulator wants to know the opinions on this proposal of “listed issuers who may wish to issue green, social, sustainability or sustainability-linked (GSSS) bonds, as well as investors and any other interested parties” (Consultation, frontispiece).

In essence, the FMA is seeking to bootstrap a bigger market for listed retail green bonds in New Zealand and inviting input from potential players on how best to go about this expansionary project through disclosure exemption. To pique interest, the Consultation repeatedly refers to climate reporting entities (CREs) and their obligations with respect to climate statements and climate transition plans as a heavy hint as to who some of the customers might be for the FMA’s proposed class exemption. CREs are going to need to raise funds in order to help realise transition plans for achieving a low carbon economy and finance activities linked with mitigations and adaptations required in response to climate change.

It could well be that once the proposed class exemption is granted, the FMA will effectively detonate the “big bang” that the Information Sheet failed to do, but only actual supply and demand thereafter will tell. Part of what the Consultation is seeking are indications of the market forces that might be unleashed upon listed retail green bond issuance when spurred on by a class exemption. In this sense, the Consultation is testing the hypothetical proposition that if PDSs were not required, then presumed pent up supply and demand for listed retail green bonds would be unleashed.

The technical aspects of how the FMA proposes to go about the procedure of creating the class exemption it is consulting upon can be left to the reader to absorb from the Consultation itself. For the purposes of this article, the Consultation will be analysed further in relation to three topics:

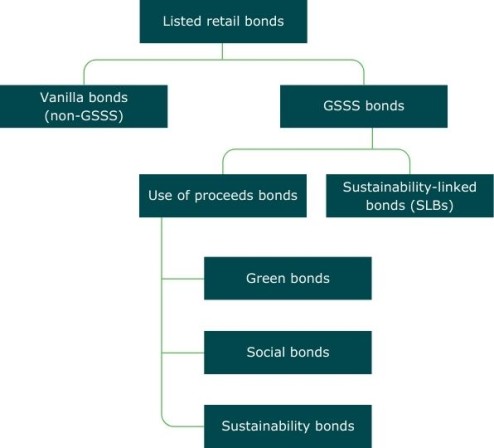

A striking feature of the Consultation relative to the likes of the Information Sheet is how it sets out a clear-cut taxonomy for listed retail bonds in New Zealand. The Information Sheet applies a fairly loose description of what green bonds are:

Green bonds are a subset of the wider category of “responsible” or “sustainable” integrated financial products that expressly incorporate a very wide range of possible non-financial factors. While this information sheet focuses solely on green bonds, the principles outlined below can extend to other types of responsible and sustainable investment products (e.g. bonds labelled as social, impact, sustainable etc.).

(Information Sheet, p. 1).

The Consultation tightens up the Information Sheet’s description significantly by relying upon a series of discrete definitions for five categories of bonds: vanilla, green, social, sustainability and sustainability-linked. The latter four bond categories are collectively referred to as GSSS bonds in the Consultation, which is concerned with granting a class exemption for GSSS bonds only. GSSS bonds all share in common that they are integrated financial products (IFPs) that have “a component that offers investors a non-financial benefit, relating to advertised environmentally or socially responsible aspects of the product” (Consultation, p. 2). Vanilla bonds are simply defined negatively as not being GSSS bonds. GSSS bonds, in turn, break down into two quite distinctly different groups, which can be dubbed “GSS” (green, social, sustainability) for one group and “S” (sustainability-linked) for the other.

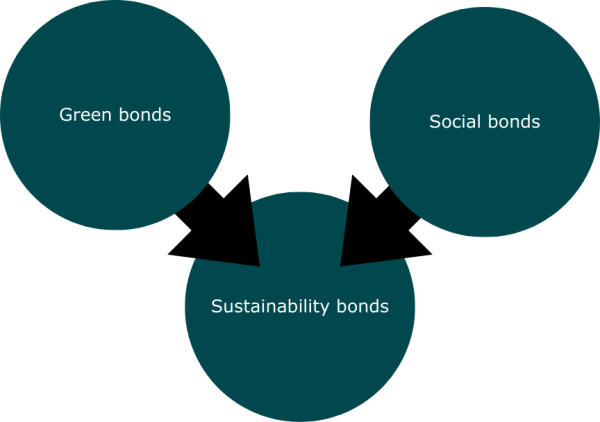

In the GSS group, green, social and sustainability bonds are clustered together for sharing in common that they are “use of proceeds” bonds, “where the proceeds are committed to a project the issuer considers to have a positive environmental or social benefit” (Ibid.). Green and social bonds are classified as being of two independent types. Use of proceeds bonds that combine both green and social components together within the same bond are assigned to a third, derivative categorisation as sustainability bonds. The definitions provided for the GSS group of bonds are short and succinct:

Green bonds – bonds where the proceeds will be used to finance or refinance environmentally friendly projects or assets

Social bonds – bonds where the proceeds will be used to finance or refinance projects or assets with positive social outcomes, or to address a social issue

Sustainability bonds – bonds where the proceeds will be used to finance or refinance a combination of green and social projects or assets.

(Ibid.)

Curiously, the Consultation states of use of proceeds bonds that:

Frequently, the commitments made by the issuer in relation to use of proceeds bonds do not represent a contractual obligation on issuers. This means it is possible for the bond to lose its status as ‘green’, ‘sustainable’ etc (for example if the proceeds are not allocated as originally intended, making it misleading to continue to describe the bond as ‘green’), without amounting to a default by the issuer or giving rise to any rights for investors.

(Ibid.)

Use of proceeds bonds may not necessarily retain the green, social or sustainability characteristics that their investors first expected, and there may be no adverse consequences for the issuer or recourse for the investors, provided the bonds are not misdescribed at any time. This fact might come as a surprise to investors, although the FMA does not appear to be concerned.

The S group of bonds is rather confusingly called sustainability-linked, yet neither belongs to nor is linked with the sustainability bonds group or, more generally, the use of proceeds/GSS bonds grouping. A fundamental reason for the S group to be separate from the GSS group is that its bonds are not of the use of proceeds type. The Consultation defines sustainability-linked bonds at greater length than it does the GSS group’s bond types:

These are bonds where the financial and structural characteristics may vary according to the issuer’s progress against certain objectives, often called sustainability performance targets (SPTs), that are predefined by the issuer. This is usually intended to penalise the issuer if they have not made sufficient progress against their sustainability goals, most commonly by increasing the interest rate it must pay to investors, making the cost of raising the capital more expensive.

Therefore, while a sustainability-linked bond offers a non-financial benefit to investors in terms of the issuer’s sustainability commitments, if the issuer fails to meet its targets, depending on the structure of the sustainability-linked bond, the investor may benefit financially in terms of the overall bond yield.

Sustainability-linked bonds (SLBs) differ from use of proceeds bonds in that the money they raise is not expressly committed to funding the realisation of any green, social or sustainability goal. Instead SLBs are linked to the issuer successfully undertaking contingent actions related to improving sustainability. Funds raised by SLBs may not even be invested in any sustainability endeavour. Unlike use of proceeds bonds, if the SLB issuer does not realise its sustainability objectives, then it has a price to pay, and investors receive the benefit. The Consultation notes:

When selecting their objectives or SPTs, issuers also often identify a set of key performance indicators (KPIs), which may be used to measure performance against the SPT, or which may themselves be linked to whether the financial or structural variations to the bond are triggered.

Funds raised by SLBs do not usually have any restrictions relating to use of proceeds, and are allocated towards general corporate purposes. They may be popular with issuers that do not have existing green assets or projects (for example, because they are at the beginning of their climate transition). They also impose actionable green obligations on issuers (as opposed to typical use of proceeds bonds).

(Ibid. pp. 2-3)

Unlike use of proceeds bonds, SLBs come with contractual obligations upon their issuers to meet stated SPTs on pain of financial penalty for failure to do so. On the other side of the coin, investors in SLBs are rewarded financially for issuers’ failures to achieve SPTs. A penalty interest rate paid out on an SLB represents a windfall for investors who bought the bond at a lower yield. Cynics might argue that that is precisely why investors should buy such bonds because if an SLB was good enough to purchase at the outset, it only gets even better when its SPTs are missed. The interest penalty represents a case of an implied price for a non-financial benefit, as it is paid as deprivation compensation in lieu of the SPTs not being attained. Arguably, the monetary value of the SPTs to investors is the price of their non-fulfilment interest penalty.

Potentially, the particular case of SLBs with their SPTs subject to penalty clauses mandating deprivation compensation paid to investors for non-fulfilment could serve as a model for valuing the non-financial benefits (alternatively, non-financial factors or NFFs) of other IFPs on the assumption of calculating a theoretical monetary compensation value for loss of such benefits. For example, for the potential value, if any, of NFFs that could be foregone if a use of proceeds bond were to lose its green, social or sustainability status, as the Consultation envisages is possible. Such an approach might also be extrapolated to managed funds marketed as having GSSS-type NFFs. The basic idea is that if investors are hypothetically regarded as being deprived in part or whole of the benefit of the NFFs attaching to an IFP, then it should be possible to calculate a compensation value for the loss that amounts to what the NFFs are adding as return on the investment.

The diagram below illustrates how the Consultation’s schematic taxonomy of listed retail bonds is set up.

The taxonomy is helpful for investors who are trying to understand and make informed investment decisions about the listed retail bond market in New Zealand. Whatever the GSSS bond on offer, it should be possible to work out:

The taxonomy dissipates a lot of the fog around what “green bonds”, a vague generic term, actually crystalizes into when it comes to investors parting with their money.

The taxonomy’s approach could be beneficially applied to other IFPs, such as managed funds, to see where they fit in the green scheme of things. Issuers of IFPs and their Supervisors can also potentially extract value out of using the taxonomy or something like it as a means to help determine whether the language used in the disclosure and advertising of such financial products is fully compliant with the requirements of the FMC Act.

The Consultation repeatedly refers to the FMA’s December 2020 guidance note Disclosure framework for integrated financial products (Guidance Note), which is largely concerned with FMC Act fair dealing and disclosure considerations as they relate to IFPs. These references serve to reinforce the continuing relevance and importance of the Guidance Note to the FMA’s current thinking around GSSS bonds and by extension to IFPs in general. The Consultation implicitly references the Guidance Note’s concern with the fair dealing requirements of Part 2 of the FMC Act, where, in outlining “GSSS bond frameworks”, it states:

A bond framework for green, social, sustainability, or sustainability-linked bonds (referred to collectively in this consultation document as a GSSS bond framework) is a common tool used by issuers to communicate to investors how they intend to issue and manage their green or otherwise socially responsible bonds. It may contain information that informs how proceeds are allocated and how the issuer intends to monitor and report progress against any sustainability-related goals they have set for themselves. However, it typically does not form part of the contractual terms of the bond.

The use of a framework is derived from industry-led standards. While there are no direct requirements in the FMC Act to produce a GSSS bond framework document, doing so supports compliance with the fair dealing provisions in Part 2 of the FMC Act [our emphasis], and has become common practice among issuers.

(Ibid. p3)

Notably, the Consultation continues on to make explicit references to the Guidance Note as being relevant to the proposed class exemption, such as where it states:

The [GSSS bonds class] exemption would likely need to be accompanied by conditions requiring issuers to disclose the basis upon which their products are labelled green, sustainable or otherwise, in line with the FMA’s Disclosure framework for integrated financial products (IFPs), to fill any information gaps resulting from the bonds being issued without a PDS.

(Ibid. p. 6)

And further:

The FMA’s Disclosure Framework for Integrated Financial Products provides issuers with guidance about how to ensure investors receive useful information to aid decision-making, and we propose that conditions to this exemption will also require disclosures that will help mitigate greenwashing.

(Ibid. p. 10)

A useful summary of what the Guidance Note requires is to be found near the end of the Consultation in relation to “Conditions requiring disclosure of the additional GSSS features of the bond”:

Any exemption will also likely include additional conditions requiring the issuer to provide investors with information setting out the additional GSSS features of the bond and the basis upon which it is labelled as GSSS.

This information should enable investors to understand the value proposition attached to the instrument (in contrast to the vanilla bond), and the incentives on the issuer to meet any green or socially responsible ambitions. We consider the disclosures should address the following themes, in line with the FMA’s Disclosure Framework for Integrated Financial Products:

We are interested to hear how potential users of this exemption propose to make this information available to investors, to help inform the kind of conditions attached to any exemption.

(Ibid. p. 13)

The list of conditions for GSSS bonds confirms that the Guidance Note remains very much in force and is equally applicable as a list of essential requirements for any IFPs, be they bonds or managed funds, with or without any FMA-granted exemptions. In this regard, the Consultation will retain usefulness beyond its submission deadline.

Managed investment scheme (MIS) managers, with some limited exceptions, are this year facing their second annual round of VfM assessments for each managed fund that they issue. The applicable FMA guidance document is Managed fund fees and value for money (VfM Guidance), first published in April 2021. The VfM Guidance requires that MIS managers should undertake “regular reviews” of scheme and fund fees:

Reviewing fees and value for money should be a continuous process. We expect managers and supervisors of all managed schemes to regularly review fees with members’ best interests as the overarching consideration. Failure to carry out regular reviews increases the risk that the scheme is poor value and/or its fees are unreasonable, and that the manager is failing to meet its FMC Act obligations – consequently increasing the risk of an FMA response.

(VfM Guidance, p. 4)

The VfM Guidance sets out two situations in which regular reviews of managed fund fees VfM should occur:

Regular reviews should consist of:

We expect managers and supervisors to provide us with evidence of these reviews, and strongly encourage schemes to report the results of the reviews to their members in an appropriate form.

(Ibid.)

With respect to managed funds that are IFPs by virtue of featuring NFFs, the VfM Guidance has the following to say in relation to “Other value-adding services”:

We recognise that services other than advice can provide value for money to members. This guidance regards broader services as valuable if they add value to the member’s account – either financially, or by better aligning the scheme with member values or non-financial expectations, and ideally both. Like advice, offering a service does not mean it has value to members …

(Ibid. p. 11)

The above passage raises the question of how an IFP-managed fund’s NFFs are to be reviewed and assessed for VfM, notwithstanding that NFFs are, by definition, non-financial. This question will no doubt exercise the minds of MIS managers as they perform their 2024 annual round of VfM reviews, although they will already have gone through that procedure before, during the inaugural 2023 annual round.

The Consultation is not concerned with managed funds but does, as noted above, touch on how NFFs could have a monetary value, or at least a “value proposition attached to the instrument (in contrast to the vanilla bond)”. The clearest cut case is where a listed retail bond is an S group SLB that carries a penalty interest rate loading triggered by the bond’s issuer failing to achieve its SPTs. Implicitly, the GSS group’s use of money bonds could also have a monetary value attached to their green, social or sustainability NFFs on the assumption that investors incur a loss if the bonds’ IFP status is removed.

On the basis that what is sauce for the goose is sauce for the gander, the words “managed fund” could be substituted for the word “bond” in bullet points taken from the Consultation to read as follows concerning the value to be assessed for IFP managed fund NFFs:

In the latest annual VfM round MIS managers and their Supervisors are likely to be taking a closer look at just how the value of NFFs cashes out or, in other ways, can be objectively valued in relation to the VfM of managed fund fees. The Consultation provides some useful prompts in that regard, especially in relation to additional NFF value provided over and above a vanilla managed fund offering, measurement and reporting of non-financial performance, risks, and costs of NFFs, and consequences of failure to achieve NFF objectives.

“The FMA’s Consultation concerning a potential class exemption from PDS disclosure for listed retail GSSS bond issuers signifies a promising avenue for increasing the size and opportunities of New Zealand’s financial markets to the benefit of investors,” said Matthew Band, General Manager of Trustees Corporate Supervision at Trustees Executors.

“As the Supervisor of listed debt issuers, Trustees Executors can see the merit of the FMA’s proposal.”

“The Consultation raises other matters of great interest concerning “green” investments, such as the straightforward listed retail bond taxonomy it outlines, which helps to sort out bonds according to their vanilla or GSSS characteristics.”

“There can potentially be wider application of this kind of taxonomy across other IFP types such as managed funds to help better understand them.”

“The document serves to emphasise the continuing currency and importance of the FMA’s December 2020 Guidance Note on disclosure requirements for IFPs.”

“Issuers of IFPs will overlook or ignore the Guidance Note at their peril”.

“The VfM dimensions of the Consultation concerned with valuation of NFFs of IFPs are timely considering that MIS managers are engaging with their second annual round of VfM assessments of their schemes and funds, which Supervisors will also be involved with.”

“Just how the NFFs of IFP-managed funds will be treated this year within the context of VfM assessments will be a likely point of Supervisor attention.”

For comment or more information or to be added to the free email subscriber list of “The Supervisor”, please contact Matt Band at [email protected].