Sep 9, 2020

During the months of February and March Trustees Executors processed 10-15 times the normal number of fund switch requests for KiwiSaver schemes that it administers (around 800,000 accounts). Over this time the top 50 companies on the New Zealand stock market, as measured by the S&P/NZX50 Index, fell by around 27% from their February peak. Overseas markets experienced the same trends; for example, the top 500 companies listed in the US as measured by the S&P500 Index fell around 34% (in US dollars) from their February peak.

Markets fall in situations like this because investors sell assets at any price. Whether the asset is a fund in a KiwiSaver account, a listed index fund, an unlisted unit trust, a listed exchange traded fund (ETF) or a listed direct share or bond.

Whenever a fund is sold the underlying asset needs to be sold to pay out cash to the holder of the fund. In the case of the KiwiSaver investors mentioned above they were mainly selling Balanced or Growth-oriented funds that hold mostly growth assets such as shares and property and switching into Defensive or Conservative funds that hold mainly cash and bonds. The assets of the latter types of funds are more stable but also have lower returns in the longer run.

What we saw was the ‘herd’ on the move, individual investors acting almost in unison selling investment assets in what took on the characteristics of a panic stampede in the third week of March.

What was equally remarkable was the rapid climb in markets following the steep falls up to the 23rd of March. The New Zealand and US markets recovered rapidly to be up by around 25% by the end of June.

The investors that sold during February and March would have lost heavily if they had not bought back into their positions quickly. Even if original holdings were re-purchased once markets had stabilised it would likely take quite a long time for investors to recover their losses. Market history shows that many of these people will wait even longer to re-enter the market, probably somewhere near the next high point.

During situations like those experienced recently, our aim as financial advisers and professional investors is to ensure our clients do not run with the herd. This can add substantial value to clients in the medium to long term.

Recent studies show those who seek advice have better outcomes

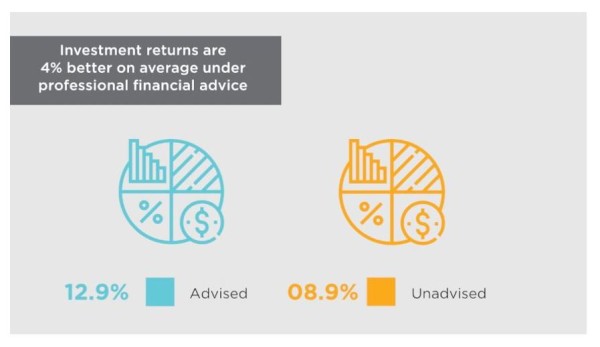

In a recent study by the Financial Services Council (FSC) “Money and You” that was sponsored by Trustees Executors, the findings show that people who use financial advisers consistently outperform those who do not. Compared to those who go it alone, they receive 4% better investment returns, save 3.7% more of their earnings, and have 50% more money in their KiwiSaver account.

Additionally, a study by Russell Investments, an international investment consultancy and fund manager, attempted to identify the value that advice can generate in their “2019 Value of an Adviser Report”. Preventing behavioural mistakes like running with the herd was estimated to add 1.9% per annum to returns.

Furthermore, ensuring clients’ portfolios are well matched to their willingness to take on investment risk was estimated to add 2.9% per annum to returns. Setting a plan and getting clients to stick with it through thick and thin pays off.

Given these compelling value-adds why don’t more investors seek advice? And if they have, are they getting the attention needed to give them the best chance of the gains that The FSC and Russell Investments have identified?

In law, medicine, accounting and other professions there are practitioners with differing specialities and business models. And so it is with financial and investment advisers. Despite the differing business models or specialties that financial advisers offer, one characteristic that all people should reasonably expect is good service, and a reasonable share of their adviser’s time. But is this always the case? Do clients always get value for money? What should an adviser be doing for their clients?

Create a Personalised Plan

One fundament to all advice is to ensure you have a plan. This provides a point of reference for a lot of decisions further down the track. The following checklist sets out in brief what should flow into, out of, and back into the plan:

- An in-depth process of uncovering what the client is trying to achieve, and when and what funding is required to support achieving these aims. The plan should be written down;

- Examination of who does, and possibly should, own the assets;

- On-going asset allocation and investment selection;

- An ability and willingness to prepare a customised portfolio;

- Consideration of tax issues;

- Pro-active re-balancing of portfolios. This adds to returns;

- Regular, ongoing and pro-active interactions between the adviser to review and amend the plan as life events unfold. Future issues should be identified and discussed. If necessary separate funding of these should be arranged (eg: spending on ‘fun’, education and healthcare funding);

- Regular and pro-active personal interactions with your adviser to help guide you through the emotions that investing and the markets can trigger;

- Referral to and working with your other advisers such as accountants and lawyers to resolve matters that have a bearing on your aims.

A financial adviser isn’t just someone who tells you how to invest your money. Rather, their role is to help you reach both short and long term lifestyle goals. The adviser works with you to determine what you want to achieve, whether that’s building wealth, funding your retirement, paying off debts, or just reaching financial stability.

Then they work to create stable streams of income to help you realise those goals. Once those are reached, new goals can be set. This means that, on an individual level, success is best measured by whether and how well those goals are achieved. On a broader scale, however, it’s possible to look at statistics to discover the concrete benefits that financial advice offers.

How we can help

At Trustees Executors Private Wealth, we make it our business to help you meet your financial goals, whether that means protecting and optimising your existing investments, or helping you to get your finances under control for the first time. If you have any questions, or you’d like to find out how our Authorised Financial Advisers can help you meet your lifestyle goals, please talk to us today for a no-obligation free of charge consultation.

Call us on 0800 768 029 or email [email protected]