Apr 8, 2021

Asset Class Returns Over 3 Months and 12 Months

Since the onset of COVID-19, the New Zealand market looks significantly different. The reaction of markets to news of the pandemic, and in turn reactions from central banks and governments in terms of support has been unprecedented. Their swift action supported businesses and individuals through lockdowns and uncertainly. The RBNZ committed $100 billion of quantitative easing through its Large Scale Asset Purchase Programme (LSAP) and setting the Overnight Cash Rate (OCR) at 0.25% for 12 months. The RBNZ has also supported banks through its Funding for Lending Programme.

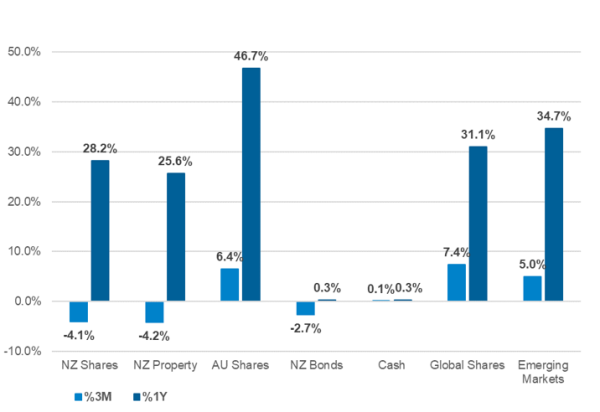

Taking the 1-year returns at face value, it appears that it was a great year of performance. Though with what we know, this is more a story of how volatile markets were and how sensitive to interest rates they are. During the COVID-19 correction, locally we saw a decline of -26% in the NZX50 (the S&P500 index declined 30%), however by the end of the year investors recovered this loss of capital and then some. The NZX50 is currently 4% higher than its pre-COVID-19 peak.

Overall, the New Zealand market returned +28.2% for the period, with information technology +138.3% (primarily Pushpay) the largest benefactor, materials (Fletcher Building) +104.1% and consumer discretionary (SkyCity and Kathmandu) +89.4%, not far behind. Consumer staples (-40.5%) and energy (-5.2%) were laggards. A2 Milk lost almost half of its market capitalisation and fell four places in the index.

Globally, the story was similar with consumer discretionary +81.7%, materials +77.6% and information technology +62.9% again the primary benefactors.

Going forward, we expect that financial markets will continue to be a volatile environment as the economy slowly reopens and vaccines are rolled out. While expectations are strongly positive, the challenge for businesses through the year will be capturing an increase in activity, after successfully cutting costs to stay afloat during the worst of the period. Markets will also be keeping a close watch on the RBNZ and interest rates, as inflation and employment data plays out.