Oct 29, 2020

- The New Zealand and US share markets reached their pre COVID-19 highs in August driven by unprecedented central bank and government stimulus, ongoing expectations of low interest rates, and resilient performance from large sectors in the stock market like technology.

- Share markets were down in September due to declines in technology stocks, second waves concern and election uncertainty.

- Interest rates continued to fall lower, and most short dated New Zealand government bonds now trade with negative yields.

What this means looking forward

- Continued volatility in shares, especially due to US and New Zealand Elections and widespread COVID-19 second waves.

- Low Interest Rates: Cash is earning close to zero. Now is the time to consider how much you need to stay in cash or if there are better options.

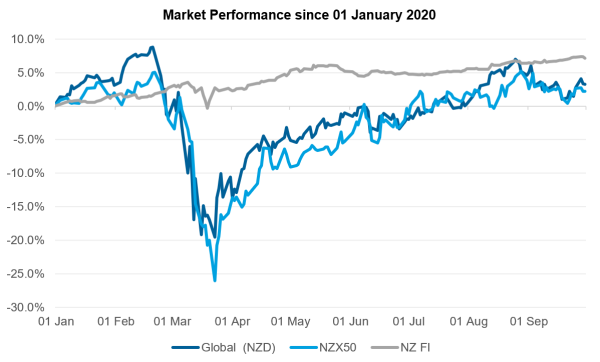

Market Summary

Since March 2020, markets have had an extraordinary recovery from their mid-March lows. To recap as you can see in the chart below there was a dramatic downturn in late February as COVID-19 spread across the world causing the quickest bear market (drop of -20%) in history. Markets turned upwards at the end of March and began a strong and steady recovery, reaching their pre COVID-19 highs in August. Some of this gain has receded in September but markets are still positive year-to-date.

The strong performance in markets can be attributed to:

Index concentration dragging markets up through August and down in September

To expand on the last point, in New Zealand a significant section of our share market is made up of Fisher & Paykel Healthcare (who make respirators) and a2 Milk (who predominantly export infant formula to China). Together these two companies make up more than 30% of the NZX50 and as such their performance has a strong impact on the performance of the NZ stock market. Both Fisher & Paykel Healthcare and a2 Milk had positive returns throughout February and March and continued to pull the performance of the NZ stock market higher. Without these two companies, the NZX50 would have a 6 month return approximately 10% lower.

In the US the index is concentrated in technology companies with Apple, Microsoft, Amazon, Google and Facebook making up about 25% of the market. While they dropped at about the same rate as the wider US market in February and March, they recovered much quicker as customers were still able to access their services during lockdown. In fact, many technology companies were more in demand from consumers as they adapted to a new digital workplace and increased time at home. These companies pulled up the overall performance of the stock market and counteracted some of the harder hit industries such as retail and tourism.

While this concentration initially worked in investors favour by towing the overall market return up, it also brought indexes down in September as tech stocks in the US and a2 Milk and Fisher & Paykel Healthcare in New Zealand had negative returns.

Shares the only game in town (pretty much) as interest rates drop

Interest rates continue to set new lows, and are expected to remain there, if not lower, for the foreseeable future. As an example of how far interest rates have dropped, the New Zealand 10-year Government bond yield was 2.6% two years ago in September 2018 and is currently about 0.5% as of the end of September.

These low interest rates are exactly what the RBNZ want in order to encourage investment, but it has also caused serious issues for people relying on deposits. Shares have ended up being almost the only option for investors seeking significant long-term returns.

If you would like to speak to one of our Trust Managers or Authorised Financial Advisers, please contact us on:

Freephone: 0800 002 478

[email protected]

www.trustees.co.nz