Nov 8, 2021

Market Review as at 31 October 2021

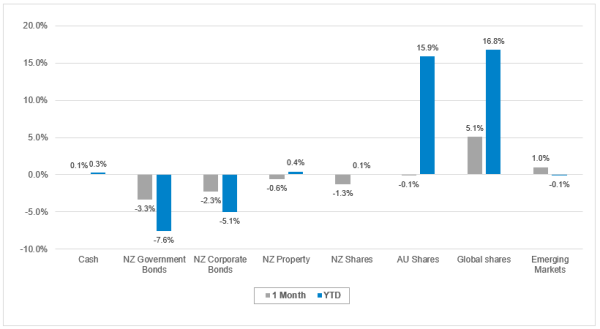

The New Zealand market fell -1.3% in October, largely on rising interest rates and uncertainty around the impact of the ongoing lockdowns in Auckland and surrounding regions. Large cap stocks had the biggest impact, particularly Mainfreight (MFT) which fell -7.2% for the month, but this follows a strong period of outperformance. Property sector declines were more modest having already been derated the previous month while Small cap companies delivered positive returns.

The main (positive) contributors to the index were Infratil, Auckland International Airport and Ebos with Mainfreight, Fisher and Paykel Healthcare and Spark providing the largest negative contributions for the month. In stock specific news, the board of Z Energy approved a takeover by ASX-listed Ampol via a scheme of arrangement, which must sell Z Energy competitor Gull to get regulatory approval for the purchase.

Looking forward regulatory concerns still hang over NZ Electricity Companies with the Government continuing to examine the feasibility of a pumped hydro storage scheme and while the Electricity Authority report on the period of high electricity prices didn’t point to a smoking gun regarding the current industry structure the option for the government to make changes remains.

Off-shore markets generally fared better than New Zealand, with the MSCI All World Index up +5.1% and the Emerging Market Index was up +1.0%. These movements reflected smaller increases in longer-term interest rates in these markets, but more importantly the shift towards the reopening of developed economies. Economic reopening progress also helped Australian equities with the S&P/ASX 200 Accumulation index ending flat over the month despite similar size increases in 10-year interest rates, as were seen in NZ.

Macro view

At a more macro level, the prior months market concerns over an Evergrande (Chinese property developer) default, European energy crisis and the US debt ceiling not being raised, abated.

However, issues remain with inflation rates globally pushing higher and central banks expected to progressively withdraw stimulatory measures as economies reopen.

On the positive side shipping costs appear to have peaked albeit high levels are expected to persist and supply constraints still remain. Adding to inflation concerns we also have OPEC ignoring calls to further increase production levels, rather sticking to already announced monthly increases end of the year.

Despite this, November has started positively with the strong start to the US third quarter corporate earnings reporting season keeping sentiment buoyant.

Fixed Interest

It was another tough month for fixed income markets. Longer-term interest rates continued to climb higher around the world as central banks signalled tighter policy settings ahead in response to reopening of economies and elevated levels of inflation. New Zealand rates however saw some of the strongest movements.

As expected, the RBNZ hiked the OCR to 0.5% however expectations of further rises this month, and the fact that the market is not discounting that it could even increase another 50bps. This meant longer term bonds increased dramatically as even should market expectations prove to be too high near term the direction is clearly for interest rate settings to continue to track higher.

As a result, New Zealand’s 5-year government bond rate increased 83 basis points and 10-year bond rates 53 basis points during October. This translated to the domestic fixed interest market falling -2.9% over the month with global declines a more modest -0.3% decline.