Nov 17, 2022

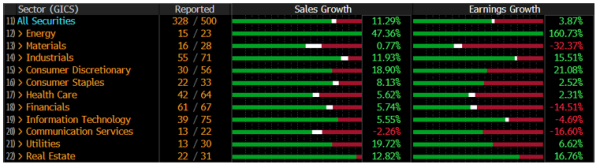

Over 65% of companies within the S&P 500 have now reported Q3 earnings and they are relatively positive. Despite all the negative headwinds which have been touted over the past year, corporate earnings are continuing to surprise the market, with cashflows remaining intact despite more expensive financing. So far, sales and earnings have grown, according to the headline figures, however, if the energy sector is removed, suddenly the picture isn’t as pretty. All sub-categories in the Energy sector have reported earnings growth for the third quarter, as it is expected to be the largest contributor to earnings growth for 2022.

According to FactSet, if the Energy sector was excluded, the S&P 500 is expected to report a y/y decline in earnings of 0.6% rather than the expected 6.1% increase. On the opposite end of the spectrum, it is a bad time to miss earnings estimates as Amazon (-9.4%) and Meta (-31.3%) experienced quick revaluations after releasing their results. Although there were some poor results, solid results from the market leaders, such as Visa (+16.6%) and McDonalds (+18.2%), provided some positive news and suggested that some companies may be better positioned for rapidly rising inflation and economic headwinds than others.

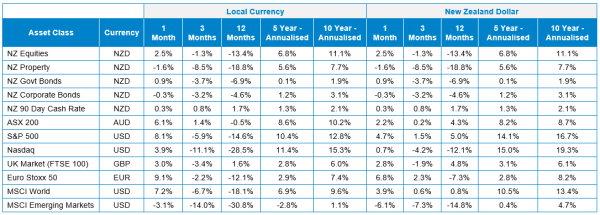

Although it has been reiterated constantly, that reining in inflation is the US Federal Reserve’s focus, markets took refuge in the idea that the FED will begin to reassess the pace of future interest rate increases. This is not to be mistaken as a pivot by the FED with interest rates expected to rise sufficiently to bring inflation back to the 2% target over the long-term. The Central Bank did note that they have entered the fine-tuning stage instead of front-loading, suggesting that future hikes will be less aggressive going forward. As expected, the FED announced a 75 basis point hike at their November meeting, with a less aggressive hike anticipated for December. A lack of surprises from the FED saw the S&P 500 gained 8.1% in October, while large-cap technology companies weighed on the Nasdaq as it underperformed gaining 3.9%. The US 10-year Government Bond ended the month lower as yields increased lower than the mid-month high of 4.3%.

New Zealand equities underperformed the global market this month, with the NZX 50 increasing by +2.46%. Tourism Holdings (+31.8%) is continuing to benefit from the reopening of the country, while an acquisition offer for $1.34 per share for PushPay (+13.6%) pushed it higher. Eroad (-18%), Pacific Edge (-14%), and Arvida Group (-12.5%) were the worst performers in the index.

The ASX 200 increased by 6.0% in October. The Financial sector (+12.2%) and the Energy Sector (+9.34%) were positive contributors with Materials (-0.1%) and Consumer Staples (-0.2%) being the only declining sectors.

Eyebrows were originally raised when the RBA issued a dovish interest rate increase of 25 basis points last month, and sceptics were proven right as inflation came in at 7.3% for Q3. Despite this, the RBA only raised rates by 25 basis points again at the beginning of November.

UK gilt yields have stabilised since Rishi Sunak became the third UK prime Minister this year, albeit they are still higher than pre-mini-budget yields, with the UK 10-year Government Bond currently at 3.39%. The FTSE underperformed the broader market, returning +2.9% in the month.

Although European companies have been underperforming year-to-date the Euro Stoxx 50 (+9.0%), Euro Stoxx 600 (+6.3%), and Germany’s DAX (+9.4%) all rose in the month. The ECB raised their deposit rate by 75 basis points at the beginning of November as inflation came in at 10.7% for October. Wheat and gas prices remain elevated as the Ukraine war continues.

Although markets were up for the month and global central banks provided few surprises, there are still significant headwinds to overcome going forward. It is clear that some companies are better equipped to weather the inflation storm, but it is important that our funds remain diversified across various sectors and geographies to ensure we are best positioned for these rebounds, as seen in October, and for any going forward.

Note: This article is meant for informational purposes only and does not constitute personalised financial advice.