Feb 12, 2024

2023 finished with a flourish, but what’s in store for 2024?

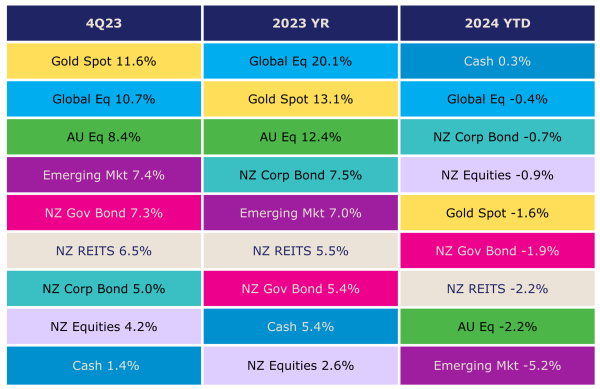

2023 turned out to be a surprisingly positive year for investors. Challenges emerged throughout the year, including the collapse of several US regional banks, heightened geopolitical tensions, and continued high interest rates and inflation. However, as we move into 2024 there are encouraging signs.

Inflation is expected to be within targeted levels in most developed countries by the end of 2024. This positive outlook set the market alight with a strong rally to finish the year in all asset classes, with Global Equities the standout.

It is only natural to expect some consolidation in the markets after strong performances in the closing months. We expect market volatility will remain throughout the year, with some major risks to watch out for. These include the oil spike from the Middle East war expanding, disruption and tension around the US election in November 24, the ensuing results, and weather events such as droughts impacting food prices and growth globally.

The NZ OCR (Official Cash Rate) is still expected to be ~4.5% by the end of year versus the current level of 5.5%, although this could change if domestic inflation continues to run above the RBNZ’s target level.

In the US it is expected at 4.0% vs. 5.5% currently. The lowering of central bank rates globally can help support growth and lead to upgrades in growth expectations, which should in turn improve companies’ earnings expectations.

TE assesses that long-term bond rates will not experience a significant decline through 2024. While some easing may be due to inflation expectations stabilising, we do not anticipate a return to the ultra-low rates witnessed in recent years. Such a scenario would necessitate implementing exceptionally easy monetary policy which is unlikely given the ongoing inflation issues. Instead, we expect bond rates to remain at their current levels, comparable to pre-Global Financial Crisis levels, both in nominal and real terms.

With this backdrop, our investment team continue to prefer investment in non-cyclical growth sectors – which are companies that are generally unaffected by economic cycles who tend to provide consistent growth regardless of whether the broader economy is in an expansion or recession phase. However, we are beginning to access cyclically exposed sectors for potential turnaround.

Overall, it is important to remain diversified across various asset classes and sectors to provide your portfolio with protection against potential headwinds and economic uncertainties.

At Trustees Private Wealth we are driven to protect our client’s financial security and support them to realise their financial aspirations. If you would like to discuss your investment portfolio and current strategy, or you are looking to invest, contact our experienced Financial Advisers, we’re here to help you.

Call us on +64 0800 878 783 or view our team below.

Chris Dilks - North Island

David Rendell - Auckland and Northland

Ann Morrell - Canterbury and Otago