Feb 27, 2024

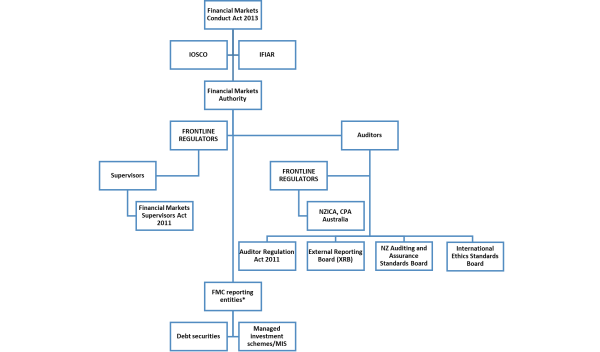

In June the Financial Markets Authority (FMA) published its latest three-year plan for audit quality reviews (“AQRs”) of licensed audit firms. The regulator is obliged to publish these plans annually no later than June 30. The Auditor Regulation and Oversight Plan 2020 – 2023 (Plan) details the work programme that the FMA has most recently set for itself, including priority themes for AQR. The auditors concerned are licensed under the Auditor Regulation Act 2011 (ARA) to perform financial statement audits for FMC reporting entities as defined under the Financial Markets Conduct Act 2013 (FMCA). FMC reporting entities cover quite a range of financial markets-linked corporates and institutions, with some of the more obvious examples including listed issuers, regulated product issuers of debt securities and managed investment schemes (MIS – think KiwiSaver schemes as the standout representatives), registered banks, licensed insurers, and even licensed supervisors, to which latter category Trustees Executors belongs.

Licensed auditors complement licensed supervisors in the FMA’s regulatory oversight superstructure for FMC reporting entities (see Chart 1). The FMA likes to refer to “frontline regulators”, meaning entities interpolated by statute between itself and the market participants it oversees and regulates. Licensed supervisors are directly counted as the FMA’s frontline regulators. In the case of licensed auditors, however, the FMA instead takes a step back and bestows the title on the professional accounting member organisations that it accredits to take responsibility for the audit oversight regime applicable to FMC reporting entities. The FMA currently recognises only two such accredited bodies: Chartered Accountants Australia and New Zealand (CA ANZ) - which it continues to refer to as the New Zealand Institute of Chartered Accountants (NZICA) for accreditation purposes - and CPA Australia.

The term “frontline regulator” is a little misleading. The entities so designated – licensed supervisors and accountancy accredited bodies - may well deputise for the FMA in applying existing FMCA-derived regulation (respectively through either direct supervision or indirectly through professional member affiliations) to FMC reporting entities on a day-to-day basis. However, such non-governmental entities have no actual authority to make, change or withdraw any regulations. In the case of the Plan, the relevant frontline regulators are the licensed auditors’ two FMA-accredited bodies. Licensed supervisors do not come in under the Plan and therefore have no frontline regulator role to perform in relation to it.

Note: *Not all FMC reporting entity types are shown in the chart. For the full list, please see section 451 of the FMCA.

The FMA reports in its Plan on how deeply embedded it is within the globalized world of auditing. Many within New Zealand’s financial sector would know that the regulator is a member of the International Organisation of Securities Commissions (IOSCO). Perhaps not so well understood is that the FMA is also one of 55 state members of the International Forum of Independent Audit Regulators (IFIAR) and currently chairs the IFIAR’s Emerging Regulators Group (ERG). The IFIAR states as its key objectives:

With this association in the background, the FMA forefronts its international role in auditing regulation in its Plan, with reference to the IFIAR’s Multilateral Memorandum of Understanding (MMOU). The overseas scope of the FMA’s auditor regulation is highlighted in the Plan’s identification of two key aims (p. 5):

Auditor regulation supports the quality and integrity of audits of FMC reporting entities. By ensuring a high standard of auditing we aim to:

Within New Zealand, over the next three years the FMA has drawn up a list of topics for reviewing selected auditors under its Plan’s working cycle (pp. 8-11):

Note: **indicates where review topics have been explicitly tagged in the Plan as needing to take account of COVID-19-related issues.

These eleven topics are described as being continued from previous areas of focus for the FMA, so should come as no surprise to auditors under the regulator’s purview. The FMA has derived the topics from international audit regulators and its own prior auditor reviews within New Zealand to create an amalgam of global and local issues to investigate under the Plan. Auditors and Supervisors may have their own preferences and recommendations for where emphasis might best be placed, such as on related party transactions, for example.

The wild card modification to the terms of the above list is inclusion of COVID-19 and what the impacts and uncertainties of this pandemic imply for New Zealand-based auditing of FMC reporting entity financial statements. In the “Our focus” section of the Plan, under “Improving audit quality” the FMA states that, “Our AQRs [ie., audit quality reviews] are risk-based, and we will consider the potential impact of COVID-19 when determining our areas of focus. Accordingly, we may change our audit quality review schedule, perform reviews of unscheduled firms, and select audit areas and audit files with a particular risk focus” (p. 3). Under “Auditing and accounting standards”, the Plan continues, “We expect that the impact of COVID-19 will be a key event that auditors need to consider when deciding on the key audit matters (KAMs) for a particular audit. Our AQR will focus on the auditor’s compliance with the standards when taking into account these impacts and changes in circumstance” (ibid.).

Of the eleven review topics for 2020 -23, the FMA has flagged in the Plan that it expects to see auditors take COVID-19 into account concerning professional scepticism, audit evidence and auditor responsibilities relating to fraud. With the advent of COVID-19, auditors are expected to manifest professional scepticism regarding “management’s assessment of going concern” and “significant judgements on accounting estimates and fair value calculations” (p. 10). Audit evidence should include consideration of new or revised risks due to COVID-19, for example in examining consequences for controls over “determining responses to identified risks of material misstatement” (ibid.). Relating to the potential interface between the pandemic and the risk of fraud, auditors should be looking at the “impact of COVID-19 when planning reliance on controls over journal entries” (p. 11). Due to profound and systemic business and economic uncertainties created by COVID-19, it should not necessarily be assumed that ramifications of the disease will wash out of auditing quality standards any time soon.

Apart from COVID-19, another new twist to the Plan is introduction of last year’s Perceptions of Audit Quality in New Zealand survey into the FMA’s worklist of tasks to tackle over 2020-23. Published in May 2019, the survey represents a first effort by the FMA at audit quality research. It is of great importance to the regulator how various sectors of society rate auditing in New Zealand. This is made plain in the words chosen for the opening paragraph of the Plan:

“The Financial Markets Authority’s main statutory objective is to promote and facilitate the development of fair, efficient and transparent financial markets. Improving audit quality, and maintaining international standards and recognition for our auditors is key in promoting trust and confidence in our capital markets, and supporting our overall objective.” (p. 3)

There were notable differences in responses to the FMA’s survey, depending on who was asked its questions. Auditors modestly rated the quality of their services very highly indeed. However, various consumers of those services - company directors, audit and risk committee (ARC) members, company managers, and investors – expressed quite a mixture of opinions and begged to differ from the auditors’ self-estimation in some significant respects. Investors showed the least esteem for New Zealand’s auditing quality, which aroused the concern of the FMA. In the Plan, the FMA sums up what it thinks auditing should represent to investors:

“Audited financial statements are a key resource for investors when making investment decisions. Investors’ confidence in financial statements is dependent on the perceived quality [our emphasis] of the audit.” (ibid.)

In the media release that accompanied publication of the survey, FMA Chief Executive Rob Everett was quoted as saying:

“Auditors have an important role to play in contributing to market integrity and informed, investor decision-making.

“While we can see that overall confidence is positive, serious expectation gaps exist among stakeholders with what they believe audit actually delivers. Our research shows that investors are not connected to the value that auditors can bring. To fill these gaps we need a concerted effort from the industry to explain their work and how they operate.

“The research also identifies the role the FMA can play to improve public understanding about the regulation and oversight of the licensed audit profession.”

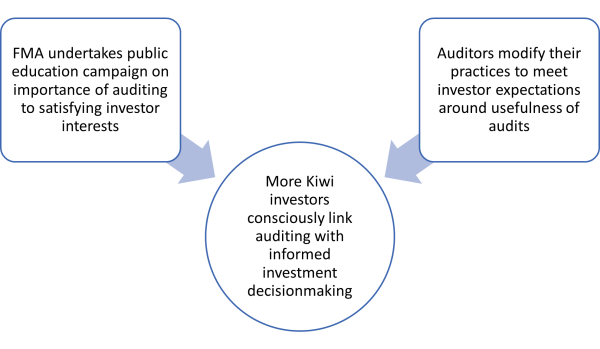

It is unclear what auditors can do to change the opinions of investors about their services or even whether such specialist service providers are sufficiently resourced and possess the communications expertise required to produce successful public education campaigns that will lead to lay persons forming improved perceptions of the quality of New Zealand’s auditing. Perhaps their accredited bodies could mount such a campaign, but again resourcing and capability come to the fore. Part of the challenge would no doubt lie in persuading more New Zealanders actually to read the audited financial statements of FMC reporting entities before investing into their public offers. Right now it is a fairly safe bet that most existing and prospective KiwiSaver investors, for example, either cannot be bothered to read audited financial statements or do not understand them properly even after making the attempt. Accountants are not necessarily the best qualified to serve as public educators and motivators for arcane and potentially offputting subjects like auditing FMC reporting entities. The FMA, by contrast, could be better positioned to do so, and appears to recognize that fact in the Plan.

Accordingly, the FMA acknowledges in the Plan a “serious gap between the expectations of investors, and what auditors are delivering” (p. 5) and sets for itself the tough job of educating investors into upgrading their views and attitudes towards the quality of New Zealand’s auditing of FMC reporting entities:

“The survey showed a gap between the expectations of investors and what auditors actually deliver. We will continue to engage with relevant stakeholders and overseas regulators to assess if changes to our audit oversight regime are required to meet our objectives. (p. 4) …

“The findings and insights from the survey can help auditors and audit firms improve how they provide assurance to investors. This is particularly important in the current challenging environment brought about by COVID-19… (p. 5)

“We will look for opportunities to communicate with investors about the nature of audited information, the oversight regime, and the role of the FMA.” (p. 12)

It is evident that as part of this nascent public education strategy, the FMA intends to make auditing practices become much more user-friendly for investors, which implies potentially significant changes to the way licensed auditors will be required to ply their trade in future. A sketch outline of this future undertaking is represented in Chart 2.

The Plan provides detailed insight into the interrelationships between the FMA, other government and overseas auditing authorities, licensed auditors and their accredited bodies, auditing of financial statements for FMC reporting entities, and the investing public. It is clear from the Plan how important audit quality is for the FMA to achieve its overarching goals. At one level, the Plan addresses eleven technical issues concerning audit quality, many of which might not seem all that significant or even understandable to outside observers not familiar with accounting practices. However, to counter the drabness and opacity that auditing may present to the public at large, the FMA has on another level committed itself to an ambitious task in putting itself forward as the primary agent of change for improving investor appreciation of the link between high quality auditing of FMC reporting entity financial statements and making informed investment decisions. This educational role will require the FMA to change auditing of FMC reporting entities in ways as yet unknown, with success of the Plan in part contingent upon unfolding uncertainties of the COVID-19 pandemic.

“As an FMA-licensed Supervisor, Trustees Executors sees the licensed auditors it works alongside with as trusted partners in ‘frontline regulation’ of FMA reporting entities,” said Matthew Band, General Manager, Trustees Corporate Supervision.

“Supervisors and auditors need to work co-operatively together under the guidance and oversight of the FMA to help ensure that New Zealand continues to evolve and refine a world class, leading edge financial markets regulatory environment that other countries could aspire to achieve.

“We support the FMA’s Auditor Regulation and Oversight Plan 2020 – 2023, not only in the eleven key topics to be examined, but also in its general public financial literacy objective of effectually linking up the work that licensed auditors do with enhancing informed investment decision making.

“While typical KiwiSaver members might not readily grasp all the technicalities of the licensed auditor’s reporting on KiwiSaver schemes they belong to, it still remains eminently desirable that they understand why auditing matters and at least how to interpret at a high level audit findings on any problems with their schemes.

“If there is one topic we as non-auditors would like to see some emphasis placed upon in the FMA’s work on the Plan over the next three years, it is related party transactions, which is an area of concern to which improved audit reporting could bring increased public benefit.”