Jul 7, 2020

Who should pay for individual unitholder transactions?

Many things no doubt got lost in the wash during COVID-19 lockdown and its aftermath, which scientists are now dubbing the great “anthropause”. One of them may have been the Financial Markets Authority’s online Fund Manager FAQs notification of May 15, 2020. Tucked away at the end of the notification was an item entitled The use and disclosure of buy/sell spreads, with the subtitle Does the FMA support the use of buy/sell spreads for [Managed Investment Schemes]? The FMA then proceeded to answer in the affirmative.

In the retail managed fund (in New Zealand, the Managed Investment Scheme/MIS) context, spreads are charges imposed to recover underlying transaction costs incurred when fund managers buy or sell fund assets in order to enable individual investors to acquire or dispose of fund units. Basically “user pays” for individual investor actions, spreads claw back trading expense, defined as meaning “the actual costs of buying and selling investments, such as brokerage fees and spreads, including those costs incurred by underlying funds” (Regulation 2, Financial Markets Conduct Regulations 2014).

Investors are charged buy spreads for buying units and sell spreads for selling units, experiencing the financial impacts of these fees via a premium on unit purchase cost and a discount on unit sale price. If funds charge spreads, they apply them to both buying and selling units, but not all funds use spreads. Funds with spreads are called “dual priced” because they have an offer (buy) price that is higher than the bid (sell) price. Funds that do not have spreads are called “single priced” because the buying and selling prices are the same.

In New Zealand it is common that retail managed funds are single priced and do not utilize spreads, instead absorbing transaction costs associated with unit purchases or sales into the wider cost structure of the fund, which is why the FMA’s opinion on the desirability of spreads is significant. The core problem being addressed by the FMA’s attention to spreads is how to maintain equity between MIS investors in the specific case where fund assets are bought or sold to help effect unit purchase or sale. Inequitable treatment can arise from “investor dilution”, wherein all of the investors in a given fund proportionally bear the transaction costs incurred by only some of the investors buying or selling units, to the net effect that all the investors involved experience decrease in the value of their holdings even if they did not personally cause those costs to arise.

Spreading the word

The FMA’s discussion of buy/sell spreads is no mere academic exercise. It is in fact a call to prompt action by MIS managers and their Supervisors. The regulator writes:

“The fundamental principle in considering the use of buy/sell spreads or any similar tool is fair treatment of investors.

“Other tools that can properly allocate those costs include swing pricing and anti-dilution levies.

“When necessary, MIS managers should work with their Supervisor to determine the tool most likely to ensure fair treatment of investors …

“Currently, not all governing documents provide for the use of buy/sell spreads or other tools such as swing pricing or anti-dilution levies. MIS managers should consider if those governing documents should be amended to allow for their use if needed…

“The FMA will monitor the implementation and level of buy/sell spreads in conjunction with MIS Supervisors.”

The FMA’s recommendation of buy/sell spreads (or swing pricing and anti-dilution levies as alternatives) for New Zealand-domiciled managed funds as a “liquidity management tool” is posed not so much as “nice to have” but rather as “when can you start?” There is also the implication that if MIS managers (including KiwiSaver managers) do not intend to introduce buy/sell spreads or their equivalents for their funds, then they will need to have sound reasons, ideally backed up by sufficient evidence, to provide to their Supervisors and the regulator. Simply ignoring the subject is not the desired response, it seems.

It is recommended that MIS managers consult the May Fund Manager FAQs to see what might potentially affect their fund offerings concerning buy/sell spreads, even if their funds charge spreads already. For single-priced funds, adopting spreads would mean shifting to dual pricing. For funds that already charge spreads, their methodology of calculating dual pricing could come under challenge. According to the FMA’s analysis, setting spreads is not as simple as a rough-and-ready calculus of what sounds about right to charge. Buy/sell spreads need to be justified from empirical evidence of what actual trading expense is incurred in executing individual investor actions, should be calculated separately for the buy and the sell sides respectively, and be subject to ongoing updating and amendment depending on how actual trading expense fluctuates over time.

The FMA frames the issue in terms of fairness to fund investors, whether or not they are the ones initiating individual investor actions:

“Depending on market conditions, costs may be skewed towards buying assets or towards selling assets. In such scenarios buy spreads and sell spreads should be separately determined to ensure they reflect trading costs incurred due to the relevant investor action (buy or sell).

“Since the spread is meant to allocate trading costs to the appropriate investor, and to prevent ongoing investors from subsidising transacting investors (or vice versa), the spread should always be applied to the benefit of the fund and never to the benefit of the MIS manager…

“Fair treatment of all investors requires that any buy/sell spread should be maintained at an appropriate level. This implies that the MIS manager must monitor the underlying asset spreads, and the costs of fund transactions, and must adjust the spread so that it is neither too high nor too low. If it is too low, then ongoing investors are subsidising transacting investors. If it is too high, then transacting investors are subsidising ongoing investors.”

Not all MIS managers agree with having spreads for their funds. As a transaction fee, a spread might not accurately reflect underlying fund trading activity. Brokerage and other costs can vary between trades. Simultaneous applications for and redemptions from the same fund can be offset by the fund manager swapping cash and fund assets between investors without incurring external transaction costs. Actual transactional costs at institutional rates for fund assets might be so low in any event as to be non-material, even during a run on a fund. In other words, spreads may not in all instances truly represent actual asset trading costs associated with individual investor actions, especially at the extreme where no such costs have been incurred. Nonetheless, trading costs triggered by investors moving their money in or out of a fund must fall somewhere and be paid by someone, which is where the issue of fairness between investors in such situations arises.

What are the alternatives?

Although the Fund Manager FAQs twice mention swing pricing and anti-dilution levies as alternatives to spreads, nothing further is said about them in context. Presumably, however, if a MIS manager were to consider either swing pricing or anti-dilution levies as substitutes for spreads, then the FMA would not object. One clue as to the FMA’s interest in spreads, swing pricing and anti-dilution levies has to do with its description of all these as a “liquidity management tool”, which points in the direction of the FMA’s current concerns around “managing [fund] liquidity risk at times of heightened market uncertainty and volatility” as stated in its media release of 17 April 2020, issued during COVID-19 lockdown. The good practice guide for MIS announced in the media release, Liquidity risk management, is more forthcoming in detail.

Under the heading “Principle 7 – Liquidity management tools” (LMTs), the guide (p. 12) is more explicit as to the FMA’s meaning in the Fund Manager FAQs:

The MIS Manager should have a range of LMTs readily available to deploy in specific circumstances, including the following …

Protecting the interests of ongoing investors, e.g. removing ‘first-mover’ advantage by having costs borne by redeeming investors, e.g. anti-dilution levies and ‘swing-pricing’.

It is important for managers to bear in mind that liquidity management includes ensuring that redemption and valuation policies and practices are fair to all scheme members at all times. Liquidity management tools, such as swing pricing and buy/sell spreads, should be used when they benefit the fund and are used to ensure that costs of trading are borne by investors driving those trades rather than by the fund as a whole. The FMA is preparing communications on this topic, which will include considerations such as disclosure and the need for ongoing consideration of the appropriateness of the spread.

Thus the importance of swing pricing and anti-dilution levies to the FMA’s thinking becomes more apparent. These techniques are intended to mitigate the risk that fund investors who get their application or (more usually) redemption requests actioned ahead of others will be advantaged by the remaining investors having to pick up the tab for the transaction costs incurred. This investor dilution problem could become particularly acute at times of market distress and dislocation, when panicked investors in a fund with falling unit values head for the exits, devil-take-the-hindmost. Swing pricing and anti-dilution levies are charges that apply to investors buying or selling units, much like spreads do. However, unlike spreads, which apply to dual-priced funds, swing pricing and anti-dilution levies are employed for single-priced funds.

Some definitions

a. Swing that price!

Swing pricing is an investor dilution adjustment technique that entails altering a fund’s net asset value (NAV) to reflect transaction costs arising from investors buying or selling fund units. The “swing” is the NAV adjustment, and when this is a set amount is called the “swing factor”. When a swing-priced fund experiences a day of net unit buying, the swing is upwards, with a premium added to NAV. When the fund undergoes a day of net unit selling, the swing is downwards and a discount is applied to NAV instead. “Full swing pricing” occurs when applied to any net unit sales or purchases that take place. “Partial swing pricing” aims to filter out non-material transaction costs associated with unit acquisition or disposal by applying a “swing threshold” beneath which level NAV adjustments are not applied. Only if the swing threshold is broached by net unit buy or sell orders would swing pricing come into effect by applying the swing factor to these transactions. Depending on market conditions, swing thresholds can be adjusted to be wider in normal times and tighter during distressed and highly volatile periods.

In a Barings white paper from November 2019, some rules around swing factors and swing thresholds are described. Swing factors and thresholds are to apply equally to all investors in a fund, although swing factors may differ for the buy or sell side of unit transactions. Swing factors may be disclosed to investors on request, but swing thresholds are withheld as confidential to prevent the swing pricing mechanism from being gamed (ie., investor dilution undertaken by deliberately pitching unit buy or sell order quantities at just below swing thresholds in order to optimise volumes bought or sold at levels which avoid associated underlying transaction costs by shifting them off onto other fund investors). Evidently the overarching purpose of these sorts of rules is to ensure fair treatment for all fund investors.

Research has been done to determine whether swing pricing works as intended. For example BIS Working Paper No. 664 “Is the price right? Swing pricing and investor redemptions” by Ulf Lewrick and Jochen Schanz (October 2017) looks at how assumptions about the efficacy of swing pricing actually bear out in the real world of open end bond mutual funds. The authors sampled bond funds offered in Luxembourg, where swing pricing was permitted at the time, versus in the United States of America, when it was then not permitted (the US Securities and Exchange Commission (SEC) amended rule 22c-1 of the Investment Company Act in November 2016 to permit swing pricing for registered open end funds except money market funds and exchange-traded funds, effective from November 2018).

The authors of the paper reached a number of conclusions concerning the redemption-side behaviour of bond funds studied (swing pricing in this case meaning that fund NAV was discounted for investor withdrawals):

The financial blog Approches Financieres in an article Swing Pricing: Swinging between Anti-Dilution and Marketing, sums up the pros and cons of swing pricing:

Pros:

Cons:

b. Levy that dilution!

An anti-dilution levy is another form of investor dilution adjustment, but whereas swing pricing applies at fund level and impacts all investors equally, an anti-dilution levy selectively targets only large transaction buying or selling of fund units and therefore applies at investor level. Functioning like a penalty charge, an anti-dilution levy would capture large standalone transactions or large aggregated smaller deals (such as wrap services undertake) and pass over smaller standalone transactions, according to UK wealth manager Charles Stanley writer Rob Morgan in an article dating from June 2019. In this manner, an anti-dilution levy functions like a filter for allocating underlying fund transaction costs either to the fund or to investors, depending on unit transaction volumes for individual orders received. A variation on this approach that commercial property funds might undertake is called “fair value pricing”, whereby withdrawals from such funds are discounted to estimated current value for selling their property assets at short notice. Like anti-dilution levies, fair value pricing can function as a deterrent to fund unit sales that would otherwise entail investor dilution.

Pros:

Cons:

Which approach to choose?

Dilution adjustments (swing pricing, anti-dilution levies) can be viable for single-priced funds as an alternative to going down the dual-priced track with spreads. Certain types of funds may be more in need of investor dilution risk mitigations than others. The Charles Stanley article suggests that anti-dilution adjustments or levies could be desirable for funds that are:

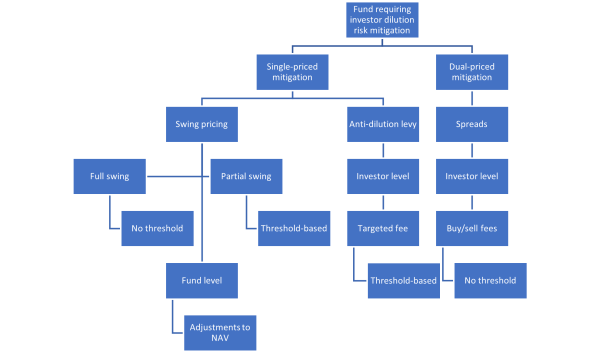

More generally, the options available are diagrammed in figure 1 below:

Figure 1: Options for MIS investor dilution mitigation strategies

How to disclose introduction of spreads, swing pricing and anti-dilution levies?

Fund Manager FAQs go into some detail concerning how spreads should be disclosed consistent with the Financial Markets Conduct Regulations 2014, including not only within the context of a fund’s product disclosure statement (PDS), but within other modes of disclosure besides. Plain English disclosure is emphasized, with the remark made that, “In our view, even the wording ‘buy spread’ or ‘sell spread’ is quite technical and wording that describes the application and effect of the spread is more likely to be effective.” However, non-technical translations of MIS industry jargon in the interests of “clear, concise and effective” disclosure could come up against word count limitation rules for PDS content and require considerable thought as to their most concise expression and where else (such as in other material information (OMI) and on websites) further descriptions could be provided.

The FMA further suggests that, “If buy/sell spreads are introduced to an existing fund, issuers should not only update their PDS and other disclosure, but should also consider how they will inform existing investors.” An article published for existing investors such as the example produced earlier this year concerning introduction of swing pricing by UK fund manager A J Bell Funds could be effective. In the case of A J Bell Funds, the change was somewhat complicated because it meant moving from an existing anti-dilution levy system over to a full swing pricing framework. Nonetheless, in the space of a short article, the announced shift in investor dilution mitigation strategy is elegantly explained within the context of investor education. Two birds are killed with one stone.

Where to next?

In its guide Liquidity risk management published mid-April, the FMA stated that further guidance would be published concerning spread disclosure and ongoing consideration of spread appropriateness. The guide placed emphasis on swing pricing and dilution levies. Come mid-May and the regulator had published its Fund Manager FAQs which indicated an expectation of MIS manager and Supervisor attention to the matter of investor dilution and appropriate unit pricing strategies to mitigate the risk. The FAQs were mostly concerned with spreads and only touched in passing on swing pricing and anti-dilution levies. The general drift appears to be that MIS managers, including KiwiSaver providers, should start thinking now about how they would prefer to address liquidity risk management and fairness to investors through investor dilution mitigation strategies.