Oct 21, 2020

Over the past few months, we have spoken about some straightforward ways to improve your financial situation so that if you are hit by a crisis such as a job loss or economic recession, you will be able to adapt and recover quickly. As a part of this series we discussed the importance of having an emergency fund, ways to get rid of bad debt, and how to pick the best KiwiSaver for your goals.

Now that you have the tools for a stable financial foundation, you might be thinking about ways to both protect against something bad happening, and also improve your life in the future.

In this final article we look at how to invest. We identify the best ways to get started, how often you should be investing and whether you should prioritise paying down your mortgage or investing in the market.

How to get started investing

To get an understanding of the concepts, a great place to start is our Investor basics article. This article gives you an investing foundation, including setting goals, diversification, and balancing risk and return.

A key part of the article is that the best time to invest is right now. Yes, take the time to do your research and make a considered decision. However, we suggest that the best thing you can do for your future self is just to get started and not try to time the market. If you’ve made the decision that you’re ready to start investing for the long term, then act now. You could be missing out on significant gains while you’re waiting for the market to get ‘better’ or ‘safer’.

How often should I invest?

Annually, quarterly, monthly, weekly, daily? The timing of investment doesn’t matter as much as making it automatic. A lot of people set up a regular investment to coincide with their pay check so they don’t even notice the money coming out of their account.

Another factor to consider is the minimum allowable investment of what you’re buying. For example, if you want to invest in a few different funds but they each have a minimum investment of $50 then you may need to invest monthly rather than weekly to account for this.

If you have extra funds building up it might be time to increase your investment amount or make a one-off investment. As always though make sure you’ve factored in any upcoming spending needs like a big trip or a house renovation.

Should I use excess funds to pay down my mortgage or invest?

This is a common question from people who have bought a home and the answer will very much depend on what is most important to you.

If you look at this question from a mathematical perspective the general rule of thumb is if the return you expect to receive on an investment is higher than the interest rate of your mortgage, you’d be better off investing. This is because the amount you are paying on mortgage is similar to a rate of a return on an investment, the only difference is one you are getting and the other you are paying. For example, if you were to put an extra $1,000 towards paying off your mortgage which has an interest rate of 3%, you would save yourself $30 that year, leaving you $30 richer. If you had invested that $1,000 and it had a return of 3% that year your investment would be worth $1,030, leaving you $30 richer.

There are several other factors to consider beyond the simple math. Below are some pros and cons of each option which will help you consider what is the best choice for you.

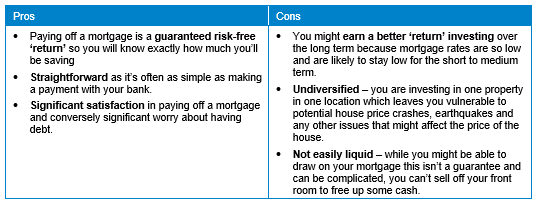

Paying off a mortgage:

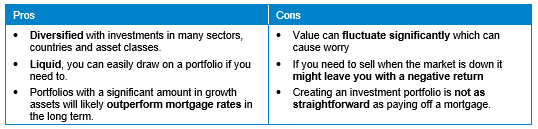

Investment portfolio

When looking at investing it will depend on what you invest in. For illustration purposes let’s assume you’re looking at an investment similar to a KiwiSaver Balanced or Growth fund. As always, we recommend investing for the long term.

A great compromise is doing a mix of both. For example, investing half of your surplus funds and putting the rest towards your mortgage. That way you are getting debt free faster while also creating a diversified, liquid portfolio that has the potential for significant growth.

As a final note, your decision doesn’t have to be set in stone, you can always change where you put your excess funds. If mortgage rates go up and you would prefer to focus paying off your mortgage, then at least you will have saved some money in an investment portfolio while rates are low. Investment portfolios also create a growing income stream over time, which could be used to pay off mortgages, kids education, retirement or whatever else you want it to.

The bottom line

It was Albert Einstein that once said ‘Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t pays it’. By starting an automatic investment you are doing your future self a favour, and setting yourself up to be prepared for any crisis.